How to Choose the Right PI Insurance for Your Accounting Practice

When you’re setting up an accounting practice, PI insurance isn’t optional — it’s a compliance requirement from your professional body. But the fact that it’s mandatory doesn’t mean all policies are equal.

The difference between a well-structured PI policy and a cheap one might not be obvious when you’re comparing premiums. It becomes obvious when you need to make a claim.

This guide walks you through what to actually compare when choosing PI insurance — beyond the price tag.

Start With the Wording, Not the Premium

The single most important thing to check in any PI policy is the wording type.

• Civil liability wording covers a broad range of claims — professional negligence, misleading conduct, breach of duty, and more. This is the standard you should expect from a specialist provider.

• Professional negligence wording is narrower. It only covers claims arising from negligent advice or services. If a claim falls outside that definition, you’re not covered.

For an accounting practice offering tax, BAS, SMSF, advisory, or audit services, civil liability wording provides meaningfully broader protection. It’s the difference between a policy that covers your actual risk profile and one that covers a subset of it.

The Six Features That Matter Most

Beyond wording type, these are the policy features that separate adequate cover from inadequate cover:

1. Retroactive Date

This determines how far back your policy covers you. An unlimited retroactive date means there’s no cut-off — all past work is covered. A limited retroactive date means claims arising from work done before a specific date aren’t covered.

If you’re transitioning from an employer’s policy to your own, this is critical. Any gap in retroactive cover leaves you exposed for advice given under your previous arrangement.

2. Reinstatements

Your cover limit applies per claim. But what happens if you have more than one claim in a policy period? Multiple reinstatements mean your limit resets — typically two or three times. Without reinstatements, one claim can exhaust your entire annual cover.

3. Defence Costs — Exclusive or Inclusive of Limit

Legal defence costs can be significant, even when a claim is ultimately dismissed. If your policy’s defence costs are inclusive of the limit, those costs reduce your remaining cover. If they’re exclusive, your full cover limit stays intact for the actual claim.

This is one of the most common ‘hidden’ differences between policies. Always check.

4. Excess on Defence Costs

Some policies charge you an excess not just on the claim itself, but also on the defence costs. That means you’re paying out of pocket twice. Look for a policy where excess applies to the claim only, not the costs of defending it.

5. Run-Off Cover

If you stop practising, claims can still arise from work you did while active. Run-off cover (or ‘tail cover’) protects you after you cease practice. For sole practitioners, this is essential — there’s no continuing firm to carry the policy.

6. Compliance Alignment

Your professional body — CPA Australia, CA ANZ, IPA, or ATMA — sets minimum PI requirements. A specialist provider builds compliance alignment into the policy structure, so you don’t have to cross-reference conditions yourself.

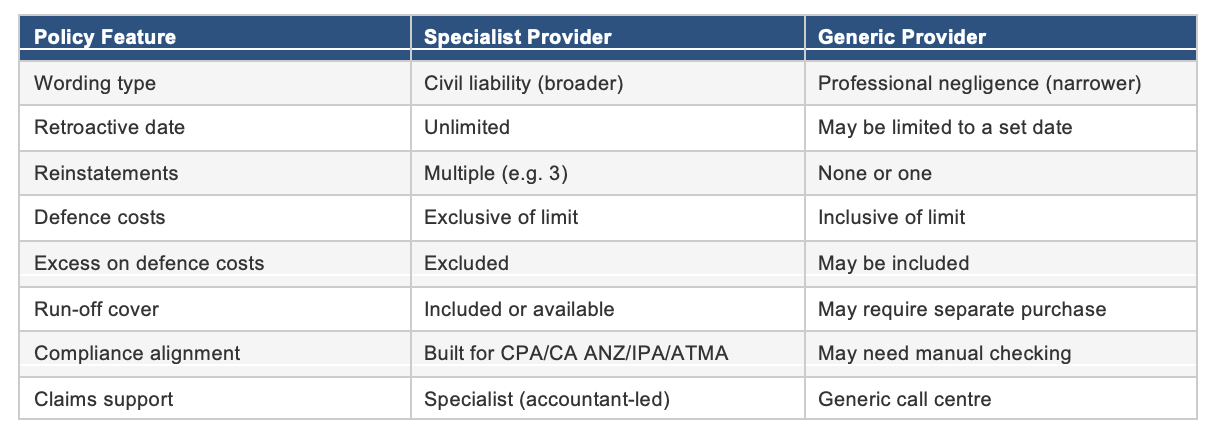

Specialist vs. Generic: A Side-by-Side Comparison

Here’s how a specialist accounting PI provider typically compares to a generic professional services insurer:

The premium difference between these two categories may be modest. The cover difference is not.

Questions to Ask Before You Commit

When you’re evaluating PI providers, these questions will surface the gaps that brochures and premium comparisons won’t:

• What type of wording does the policy use — civil liability or professional negligence?

• Is the retroactive date unlimited, or does it start from a specific date?

• How many reinstatements are included?

• Are defence costs exclusive of the cover limit?

• Is excess charged on defence costs as well as the claim?

• Does the policy include run-off cover, or is it a paid add-on?

• Is the policy structured to meet my professional body’s requirements?

• What does the claims process look like — and who handles it?

TIP: If a provider can’t clearly answer these questions, that’s a red flag. A specialist insurer should be able to walk you through each point in plain English.

Don’t Forget About Add-Ons

PI covers professional advice and services. It doesn’t cover everything. Depending on your practice, you may also want:

• Cyber insurance — for data breaches, ransomware, and email compromise. Increasingly essential for any practice holding client financial data.

• Public liability — for physical injury or property damage connected to your operations. Relevant if clients visit your office or you visit theirs.

• Statutory liability — for fines and penalties imposed by regulatory bodies.

A good provider will offer these as add-ons within a single policy framework, rather than requiring separate policies from different insurers.

How Abacus Makes Choosing Easier

Abacus Australia has been providing specialist PI insurance to accountants since 1990. Every feature listed in the ‘specialist provider’ column of the comparison table above comes standard with an Abacus policy.

That means civil liability wording, unlimited retroactive date, three reinstatements, costs exclusive of limit and excess, run-off cover, and compliance alignment with all four professional bodies — without you needing to ask.

Our accountant-led claims committee provides practical, human support when something goes wrong. Not a generic call centre.

Get an obligation-free quote from Abacus Australia. Visit www.abacusaustralia.com/getaquote or call 03 9552 0600.